NPL Outlook Europe 2021:How data-driven digital technology will help manage the tide

QUALCO, in association with DDC Financial Group, is excited to announce the launch of a special report which will address the latest and most relevant information on the NPL sector in Europe. With a particular focus on how data-driven technology will play an ever-increasing role, the report is driven by fundamental analysis on macro and micro-economics and the main trends that are affecting the outlook in this sector for the coming years. Below is what you can expect.

The Veil will soon be Lifted

Never in recent memory has so much uncertainty been hanging over global growth. Several concerns hinder global economic recovery in 2021, such as control of new variants of Covid-19, vaccine roll-out delays and inequality, and the fact that it is simply unknown just how much lasting economic damage has been wrought.

As furlough and moratorium schemes conclude, account receivables will be placed under severe stress and businesses can expect to see arrears, provisions and bad debt levels increase at unprecedented rates. Only when that support is withdrawn will the veil be lifted.

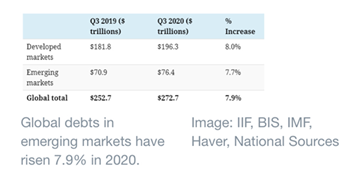

The huge rise in corporate leverage combined with an uncertain economic outlook increases the chances that debts will not be repaid in full or on time. Defaults have already picked up sharply. The global debt load increased by 19.5 trillion in 2020 and now stands above $272 trillion. Almost no one expects the economy to have fully recovered by the end of 2021, with some estimates indicating that global debt could exceed $360 trillion by 2030.

Private Debt continues to attract strong demand from global investors who have essentially gone looking for what they cannot find in public markets to meet their evolving needs. The European demand for private capital has extended to lending and, in this environment, European private credit managers and their investors, have demonstrated their commitment and expect to provide businesses with over $110 billion of new capital.

2021 - A year of acceleration of the European NPL transactions

“Investors expect European banking sector consolidation and acceleration of Non-Performing Loan (NPL) sales in 2021” Fitch Ratings says.

In addition, PwC estimates that NPL trades with a face value of around €150bn will trade in 2021 and 2022, with most taking place in 2022. During 2021 we expect much of this trading to be of legacy stock and thereafter likely to be newer stock arising from the current crisis. At the end of 2020, a total of 140 NPL deals occurred, UK with 49, France with 29, Germany with 23, and the rest of EU with 39.. The hunt for yield with strong technical values will continue further into 2021, with long-term low-interest rates, Covid related disruptions, and the attendant need for finance among borrowers likely to continue beyond 2021.

European NPL Stock Evolution and Expected Impact

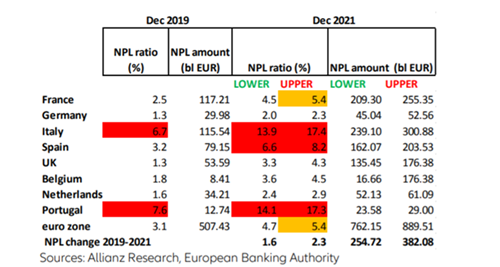

In an adverse scenario, the ECB has estimated that the amount of non-performing loans (NPLs) in the Euro area might reach €1.4 trillion by the end of 2022, while the Eurozone NPL ratio is expected to increase from 3.1% in Q4 2019 to 4.7%-5.4% by the end of 2021. This would put between EUR 255-380bn of additional NPLs on Eurozone banks’ balance sheets by the end of 2021.

The deterioration in asset quality amid rising insolvencies would surely push banks to tighten credit conditions in 2021 in Italy, Portugal, Spain, and France as well as put bank profitability under pressure in Germany, Belgium, and Portugal.

NPL loss simulations 2019-2021

On December 16th, 2020 the European Commission on Coronavirus response issued the guideline “Tackling non-performing loans (NPLs) to enable banks to support EU households and businesses” in which it identified only 21 of the 113 significant institutions were able to forecast the level their NPLs will have reached by the end of 2021. The guideline concludes that “history has shown us that it is best to tackle NPLs early and with decisive action, while ensuring robust consumer protection, to allow the banking sector to play its role in supporting the economic recovery”.

How does Technology help to avoid credit crunch and losses?

Traditionally, NPL management has not been a focus for digital technology but this pandemic crisis has clearly propelled the world into a very different future. At the same time, creditors need to reconsider vulnerability anew as millions of people are now experiencing financial insecurity and, in many cases, for the first time. As banks, lenders, and collections functions are dealing with a unique set of challenges, new tools are required to ensure fair customer outcomes and satisfaction. In that context, leveraging analytics to better understand customers’ circumstances and suggest appropriate forbearance options that can then be delivered via digital mediums such as on-line and chatbots is now a necessity. Savvy business leaders are investing now in a combination of operations automation and advanced analytics underpinned by a comprehensive collections platform to help mitigate this expected surge in impairment. Automation, on one hand, has a clear, direct impact on operational efficiency achieved by 360-degree customer views, guide scripts, dialler and digital channel integration, while advanced analytics on the other hand builds on operations to improve effectiveness through optimal segmentation, contact channel treatment selection, and action prioritisation by leveraging data recorded in the operations platforms and combining it with additional sources where appropriate.

In the full report published in next month’s issue of DDC’s Debt Business Magazine, we will delve into greater detail on these topics. Stay tuned!