1. Introduction

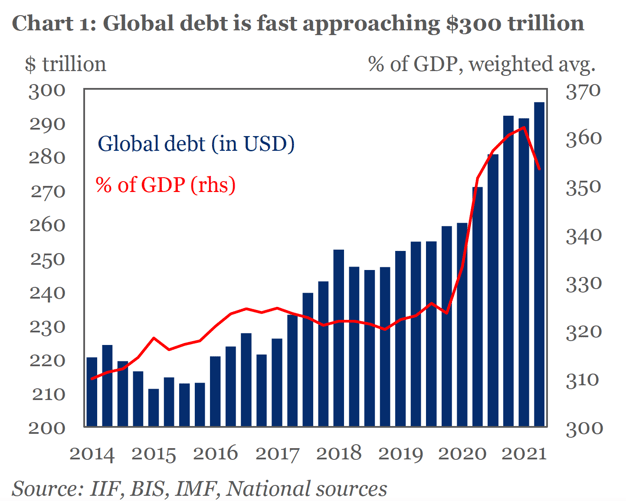

Total debt* levels around the globe rose to $296 trillion at the end of the second quarter of 2021 according to IIF, in an effort from governments to revive pandemic-hit economies. Considering the magnitude of the situation, debt management is becoming top of mind for the lending industry. Besides stimulus packages and moratoria, a more forceful approach will be needed to rise to the occasion. More specifically, with debt management practices applied by creditors, they can ensure that not only debt will stop soaring, but it will eventually start shrinking in the coming years.

*The total level includes government, household and corporate and bank debt.

2. What is debt management?

Debt management is one of the procedures that aim to empower borrowers to regain control of their finances by enabling them to handle their unsecured debt through a third-party negotiator. By opting in, the debtor allows credit counselors to work with the lenders on their behalf, negotiate lower interests and combine all payments in a single monthly payment. These processes usually last from 3 to 5 years, having as the ultimate goal the repayment of the debt from the borrower's side.

At this point, we should note that debt management plans are not loans and the debtor must stick to the predetermined payment schedule that was developed by the counselors and the creditors. These tailored plans are determined considering the customer's financial circumstances and what they can afford.

3. Different types of debt

Debt can be either secured or unsecured. According to Investopedia, the primary difference between the two is the presence or absence of collateral, which is backing the debt and a form of security to the lender against non-repayment from the borrower.

When it comes to secured debt, the borrower has offered a property that the lender can obtain in case the former is not punctual with the debt repayment. Mortgages and car loans are the most common types of that debt.

For the unsecured debt, there is no property backing the amount borrowed. The debtor gets the loan based on his good name and credit score. The most popular types of unsecured debt are credit cards, medical bills and utility bills.

While debt management plans can bring several benefits for the borrowers and the lenders alike, we should point out that they can't be applied to any type of debt. As we mentioned above, they can be applied to unsecured loans. So, if a debt falls in the secured category, mortgages or auto loans, for example, it might not be eligible for a debt management plan.

4. How does debt management work?

In most cases, the process goes as follows:

-

According to the legal framework of each country, the process can be driven either by a credit counselor that the customer has chosen, or by the lender (bank, loan servicer, DCA). In case a counselor is chosen, nonprofit or for-profit, will act as the middleman and will try to negotiate lower interest rates for the unsecured debt of the debtor. Otherwise, this specific part of the process will take place by the lender themselves. Then, both parties will create a plan according to the budget that the customer affords to pay.

-

At this point, the credit counselor or the lender are helping the customer to create a 3-5-year plan to repay their debt. The plan is always a result of the counselor's negotiations with the lender or of the lender and customer in combination with the financial situation of the borrower. This makes it a realistic option for people who have a hard time settling their debt.

From the financial institutions side, they can negotiate a customer’s retail debt after utilising a debt management software that will give them insights about the customer and their financial image. -

Next, comes the monthly payment of the borrower to the credit counseling office or the lender, including potential fees that might come up in the case of counselor. When they receive the payment, they are responsible for paying the bills on the lender, on behalf of the debtor. Otherwise, the payment is going straight to the lender.

5. Aspects of debt management

There are several reasons for a customer to get involved with a debt management plan. First, it helps borrowers make their payments on time according to their monthly available budget. Also, it enables them to improve their credit score over time by being punctual in their transactions and they are rather flexible, meaning that they can adapt to the financial circumstances of each client. However, at some point the debtor might have to work with an unknown middleman. Or, in case a payment is missed, the plan will stop being in force and the interest rates will return to where they were.

6. Debt management approaches

While debt management is a sensitive topic for customers and businesses alike, in the past few years creditors have been reinventing their processes. Their assertiveness when it comes to debt collection has been replaced by their desire to collaborate with each debtor on a more tailored basis. What's more, they have been investing in the creation of bespoke solutions for their customers in order to enable them to meet their financial obligations on time.

This effort starts with how the communication between the two parties takes place. While letters and telephones have been the norm for a very long time, the recent changes in today's customer behavior inevitably led lenders to adopt more modern ways to reach them out. Email, web chat, SMS texts or even social media are on the table as alternative communication channels. Communication is key in those cases and largely affects the outcomes.

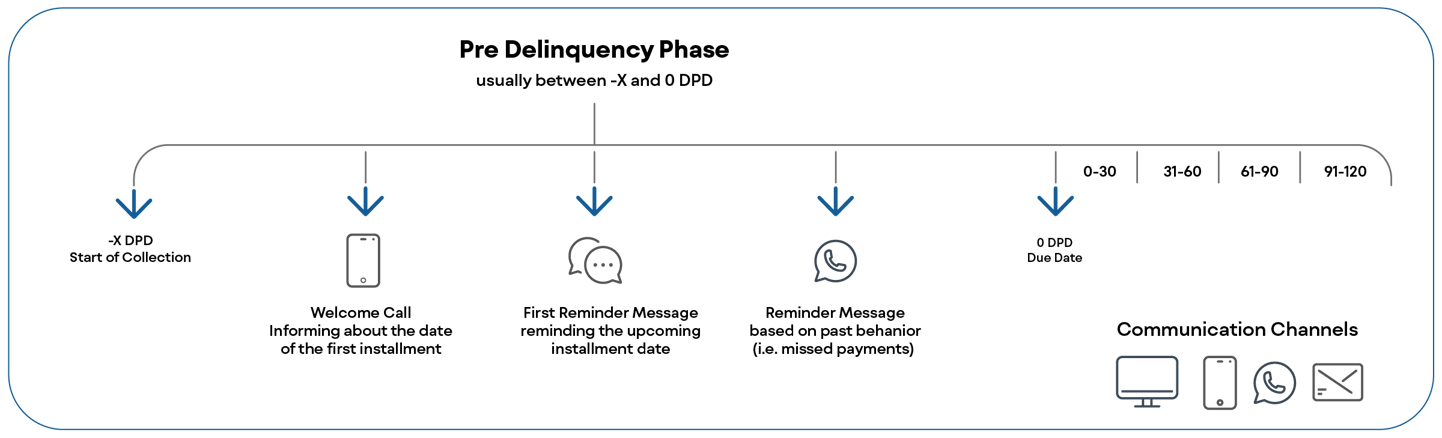

Debt management has always been a hard mountain to climb for financial institutions. The pandemic crisis has increased exposures and, in that context, creditors globally realise that detecting risk early on will enable them to preempt defaults in advance, and eventually reduce losses. This is another aspect that has been shifted. By managing to gather debt at the first stages of the customer life cycle, financial organisations will finally be able to hinder the deterioration of their portfolios.

It is worth noting that the customer life cycle adds an extra layer of complexity in the whole process since customers on the pre-delinquent phase need different treatment from those who have already defaulted. When it comes to credit risk management, history has shown repeatedly that proactive monitoring is the difference between success and failure.

For example, if lenders implement this proactive approach, they will be able to prevent missed payments at the beginning of the customer life cycle. How can this be achieved? By reaching out to them using modern channels like mobile text messages, Viber etc.

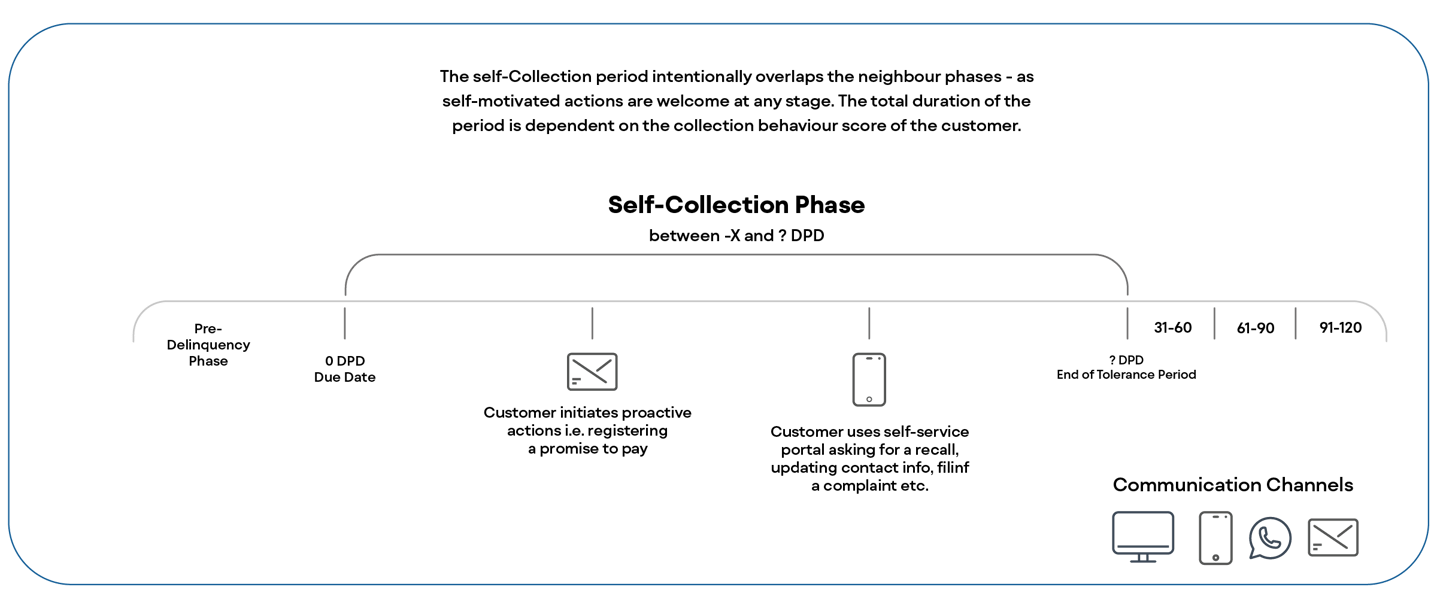

Creditors should also invest in building a strategy about the grace period, where a customer might miss a payment. This way, the customer can proactively pay off their outstanding balance before investing the organisation’s resources to contact them to make a direct request for that payment. Digital communications and self-service capabilities play an integral role in this phase.

All the above aim at shaping a better customer experience, which will lead to the reduced possibility for customers to default.

But to fill in the missing pieces and get there, lenders must leverage technology so that they can offer truly custom services that fit their customers’ specific needs.

Technology will play a crucial role here. Besides enabling the obtainment of high-quality data and indicating the proper communication channel, technology will enable the lending industry to implement the most suitable strategies swiftly for maximum efficiency. This way, the industry can respond to the constantly changing environment with minimum effort.

7. Debt Management: Differences between Debt Collection and Debt Recovery

While all 3 terms seem related, they are not the same. When it comes to debt collection and debt recovery, both include processes and activities that aim to recoup money, but they have a basic distinction. And that is who is trying to collect the debt.

For debt collection, the creditor himself is pursuing debts through emails, phone calls or other ways of reaching out to the debtor. If they are unable to achieve their goal, they either assign the debt collection to Debt Collection Agencies (DCA) or take the case at court according to the severity of the debt. Debt recovery is the process where the DCAs are assigned to recover debts on behalf of the creditor.

Debt recovery is part of the legal phase of the customer’s credit life cycle. These days, creditors can avoid reaching that stage by using data analysis and machine learning algorithms to identify early warning indicators, before a customer starts missing payments. Predictive models can be used to profile, visualise, segment, and ultimately prioritise the customers that could potentially default in order for lenders to offer tailored solutions.

8. Consumer debt management

With technology advancing at a rapid rate, creditors have started to capitalise on this progress in order to offer high quality services to their customers. With customers expecting a more human approach and experiences that match their digital lifestyle, digital collections seem to be one way and a golden ticket for the credit industry to improve its image, which has long been poor.

Digital collections, and self-service platforms more particularly, bring multiple benefits for creditors, including:

-

The streamlining of their processes and the possibility to stay compliant with new regulations. This way they can focus on activities that bring high value to a financial organisation.

-

Fewer phone calls and more time to deal with customers that show signs of distress. By spending time in high risk cases, lenders might manage to reduce the likelihood of distress.

-

Increased debt collection coming from greater flexibility when it comes to payment options. These days, it is vital for customers to be able to communicate seamlessly with their creditors and manage themselves their payment plans.

-

Improved overall customer experience by eliminating frequent and disturbing phone calls. By allowing customers to decide when and how they will interact with them, lenders are providing an enhanced and customer-centric approach.

Positive experiences are a win-win and that is why creditors need to prioritise them from now onwards.

9. Corporate and SME debt management

COVID-19 has driven European debt to a new record high with SMEs being particularly hard hit. For the past almost 2 years, the governments provide support schemes to sustain businesses, but the liabilities continue to rise.

Euro-area companies added more than €400 billion in debt over the first half of 2020, compared with €289 billion throughout the whole of 2019, according to European Union data.

The European Commission has warned that “servicing debt could be challenging particularly in sectors impacted by the pandemic in a more lasting way.” Under these circumstances, firms must now answer a critical question: How to drastically improve the management of their corporate and SME debt portfolios?

This is not a simple question to answer and corporations and SMEs need to take many aspects into consideration. The adoption of a robust debt workout framework has a lot to offer and some of the most prevalent benefits are the timely identification of the debtors experiencing business difficulties, as well as the reasons, to lead in an efficient restructuring plan.

10. The role of collections analytics

There has definitely been a fuss around data and collections analytics in the past few years. And even if creditors have started to leverage its power, the industry has a lot of space for improvement.

Today, smart companies are using data and collections analytics to identify different groups of customers and then, they interact with them in their preferred way to shape seamless customer journeys. That is how they increase both their profitability and their customers’ loyalty as well.

Also, by being able to recognise which customers are having trouble covering their financial obligations, financial institutions have the time and the data available to adapt their collections strategy and operations.

By harnessing the power of collections analytics, lenders can:

1. Tailor their debt management approaches

2. Increase their cash flow

3. Reduce their operational costs

4. Maintain a 360 view into their customer portfolio

Collections analytics is the backbone of the personalised treatment customers expect, especially around the sensitive issue of debt collection. For that reason, it is high time that financial institutions realised the value and implemented the use of analytics in their debt management strategies.

11. How QUALCO can help

Rapidly accumulating household and corporate debt has long presented a major risk to financial and economic stability. Bringing money back to the real economy requires robust debt management that reacts carefully to economic policy measures.

QUALCO offers a holistic solution for proactively managing NPLs and impaired assets.

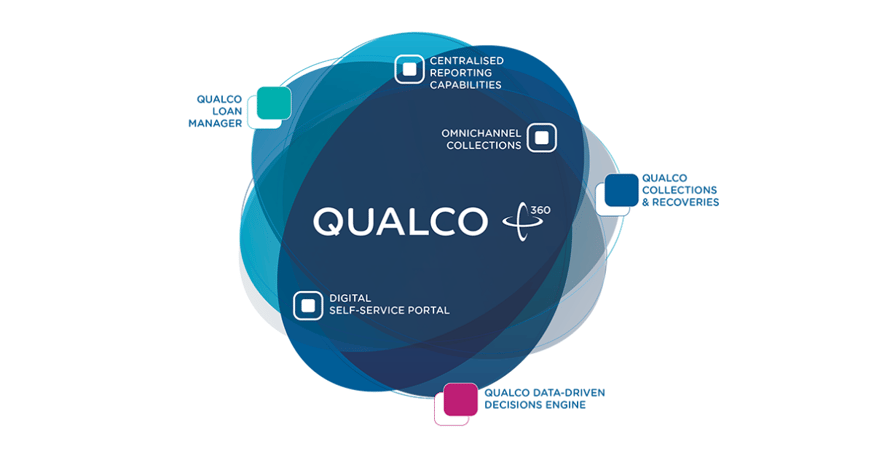

The QUALCO 360 technology ecosystem aggregates data from multiple sources and uses the best ML analytics to give creditors a 360-degree view of a customer’s past, current, and expected financial situation. It also provides omnichannel engagement tools and recommendations for debt restructuring and servicing for the best net results. Also, it enables clients to turn this data and insight into meaningful actions and credit operations, allowing the business to mitigate risks in areas of high exposure.

QUALCO 360 is a constantly expanding technology ecosystem that enables you to rapidly align operational activity with ever-changing customer behaviour. Combining analytics with ML and a comprehensive collections system, it revolutionises the management of NPLs and NPEs and radically reduces losses.

With QUALCO 360 you get:

- Greater efficiency and productivity

- Increased ROI

- Reduced Losses

- Single view of clients’ state and actions

- Streamlined information

- Seamless systems interaction

- Optimal Customer Experience