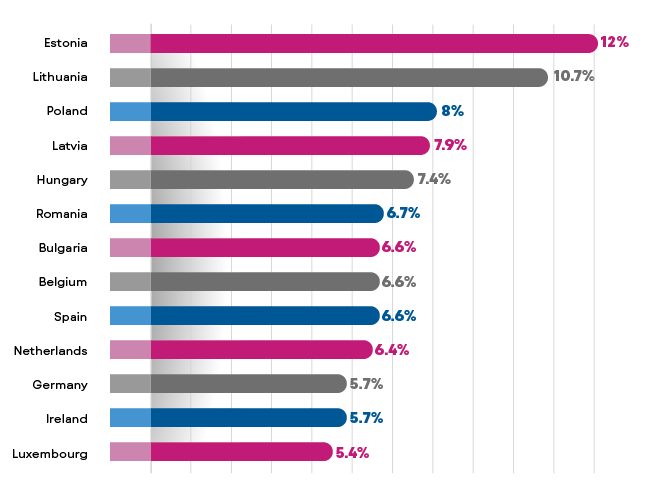

The coronavirus crisis has been an unprecedented shock that caused a steep contraction in the European economy. As inflation hit record numbers across Europe in the past months, there has been a massive increase in the cost of several products. According to research by Eurostat, inflation has soared to 4.9% on average across European countries. The following graph exhibits the highest inflation rates in several European countries:

While the wages have remained stable, a significant impact is expected on consumers and households. With their purchasing power eroding, customers will prioritise their everyday expenses over their outstanding bills, leading to a surge in NPLs.

WHAT LED TO INCREASED INFLATION

Several reasons led to higher inflation as we enter the post-Covid era. More specifically in the energy field, the increased demand during the first months of the pandemic, as well as the escalation of the conflict between Russia and Ukraine led to the inflationary crisis. As we experience the peak in the rising cost of living, analysts warn that prices might take time to readapt to the pre-pandemic levels.

Moreover, due to the strict lockdown policies and COVID-19 closures, both the supply and demand of goods and services experienced a severe drop. As a result, a significant number of consumers started to accumulate savings and liquidity mostly because they had fewer opportunities to spend. Once the global economy reopened, production activities and supply chains needed time to restart as a consequence of workers being reallocated to different jobs, a supply shortage in raw materials, and so on. On the contrary, consumers immediately redirected to newly available spending opportunities, applying a hefty demand pressure to an already stressed supply side. The combination of a slowly adjusting supply and a fast-growing demand resulted to supply bottlenecks, products unavailability, and eventually a sharp increase in prices.

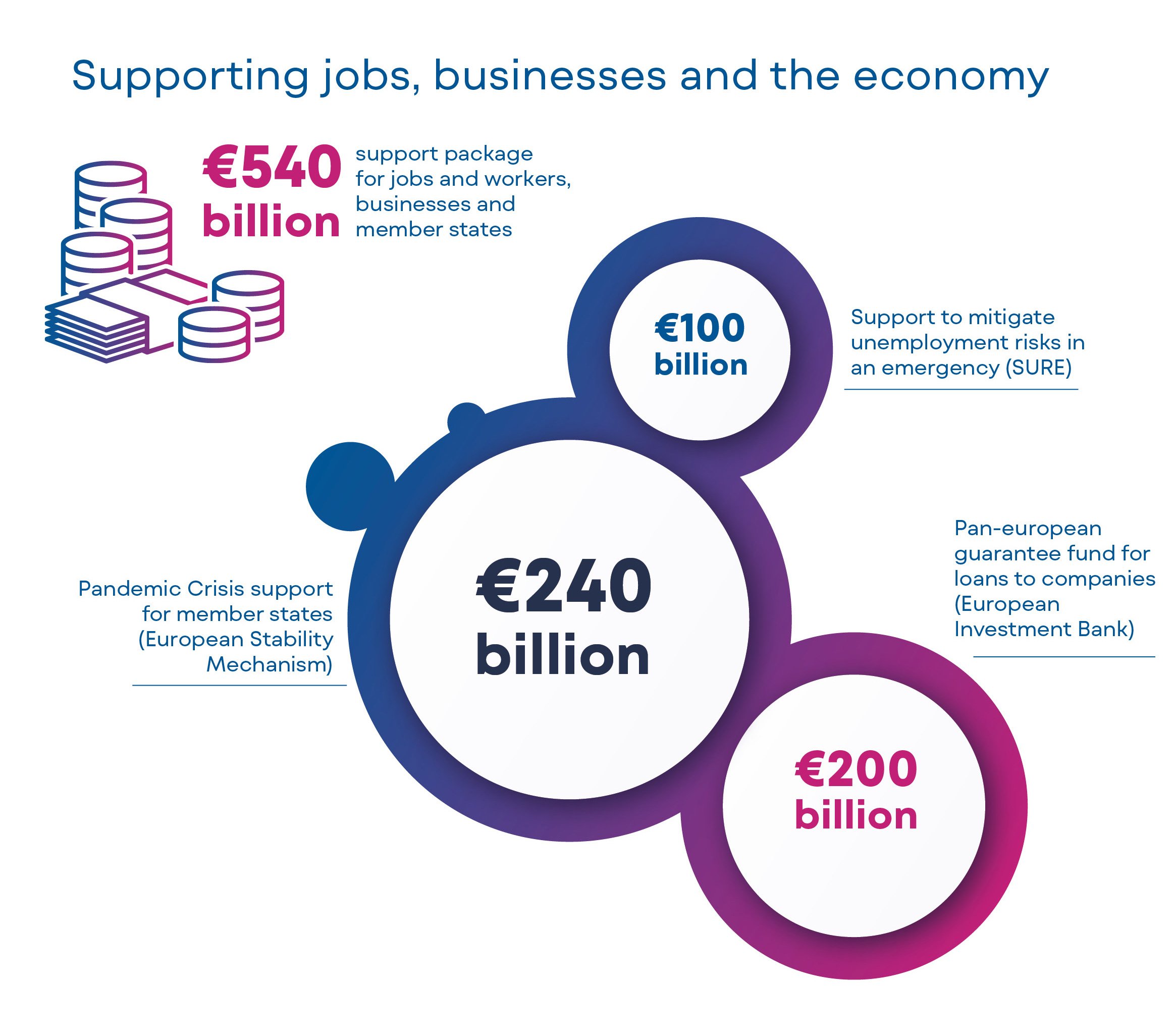

Since the onset of the pandemic, European governments have implemented several countermeasures to ensure the stability of their financial systems and mitigate the consequences of the crisis on the citizens and the economy struggling due to the imposed lockdowns. According to the European Union, 540 billion euros were leveraged for that purpose and the breakdown can be seen below:

The discontinuation of these measures contributed to the inflation increase.

WHAT THE REAL IMPACT WILL BE

Analysts predict that both the economy and the consumers’ purchasing power will be affected by this unique combination of challenges. If the phenomenon persists, consumers will be forced to become more price-conscious and deliberately reduce their spending.

Should the cost of living continue to rise at this rate in the near future, the customers’ purchasing power will continue to drop. As a result, not all borrowers will be able to meet their financial obligations and debt will escalate. This will require immediate action from the financial organisations’ side in order to bring debt on track.

WHAT BUSINESSES CAN DO

During these times and under particular circumstances, more customers and businesses are forced to increase the amount of money they borrow. Considering the fact that their purchasing power is decreasing, it is far likely that many of them will fall behind in their payments. Financial organisations will have to work toward bringing the rising debt on track.

It is of great importance that financial organisations should invest in advanced technologies, such as Machine Learning and advanced analytics, to proactively efficiently manage the increasing debt and optimise the collection process. By utilising advanced technologies and digital tools, financial institutions will be in a position to increasingly modernise debt collection and build a sound framework that will identify at-risk customers before they fall behind on payments. The power that ML brings can analyse vast quantities of varied data types and recognise the patterns that give lenders the ability for an improved evaluation of risk. Data-driven debt collections can deliver significant savings in operations and also lead to tailored treatments according to each customer’s circumstances. Leveraging the technologies that complement a holistic view of their customers will enable them in offering them the most suitable and affordable solutions.

Want to get a full grasp on the ways they can do so? Read our latest report Building a resilient Debt Management Mechanism to overcome the Rising Cost of Living.